2026 Social Security Adjustments: What a 3.5% COLA Means for Your Benefits

Anúncios

The projected 3.5% Cost-of-Living Adjustment (COLA) for 2026 Social Security benefits will directly increase monthly payments, aiming to offset inflation and maintain beneficiaries’ purchasing power.

Understanding the 2026 Social Security Changes: What a 3.5% COLA Means for Your Benefits is crucial for millions of Americans who rely on these payments. As we look ahead, the projected 3.5% Cost-of-Living Adjustment (COLA) for 2026 brings both anticipation and questions about its impact on your financial future and overall retirement planning.

Anúncios

The Basics of Social Security COLA

The Cost-of-Living Adjustment, or COLA, is a vital mechanism designed to ensure that the purchasing power of Social Security benefits doesn’t erode due to inflation. Each year, the Social Security Administration (SSA) evaluates economic data to determine if an adjustment is necessary. This adjustment is particularly significant for retirees, disabled individuals, and survivors who depend on these benefits for their daily living expenses.

Anúncios

The primary index used to calculate the COLA is the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This specific index measures changes in the prices of goods and services purchased by urban wage earners and clerical workers, providing a snapshot of inflationary pressures. The calculation compares the average CPI-W for the third quarter of the current year with the average for the third quarter of the previous year. If there’s an increase, that percentage rise becomes the COLA for the following year.

How COLA is Determined

The process for determining the COLA is meticulous and data-driven. It’s not an arbitrary decision but a calculation based on observable economic trends. Understanding this process can help beneficiaries anticipate future adjustments and plan accordingly.

- Data Collection: The Bureau of Labor Statistics (BLS) collects extensive data on consumer prices.

- CPI-W Calculation: The SSA uses the CPI-W, a subset of the broader CPI, to reflect the spending patterns of a specific demographic.

- Quarterly Comparison: The average CPI-W from July, August, and September is compared to the same period of the prior year.

- Percentage Increase: Any percentage increase directly translates into the COLA for the upcoming year.

In essence, COLA acts as a financial safeguard, aiming to keep pace with the rising cost of living. Without it, the fixed income of many beneficiaries would gradually lose value over time, making it harder to afford necessities. The projected 3.5% for 2026 signals a continued effort to protect beneficiaries from inflationary pressures, offering a degree of financial stability in an ever-changing economic landscape.

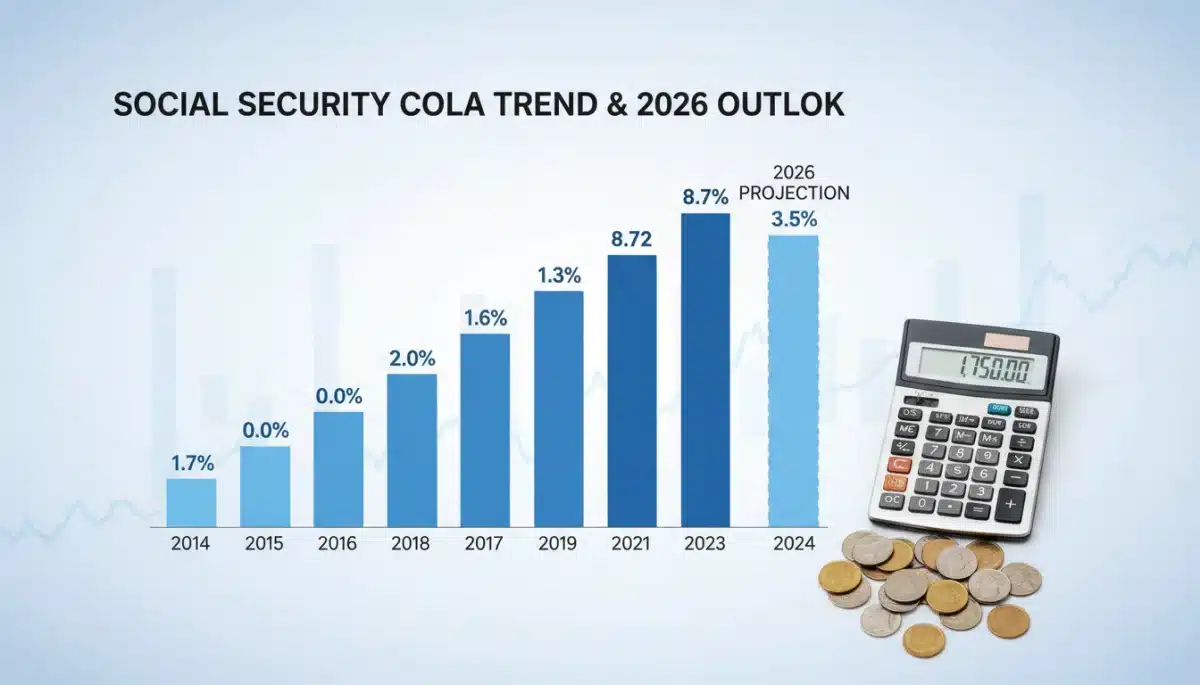

Projected 3.5% COLA for 2026: What’s Behind the Number?

The projection of a 3.5% COLA for 2026 is a significant forecast, indicating continued inflationary pressures or at least a sustained level of consumer price increases. This figure is not finalized until later in the year, usually in October, but early projections offer valuable insights for financial planning. Several economic factors contribute to this prediction, and understanding them is key to grasping the potential impact on your benefits.

Inflation, as measured by the CPI-W, is the primary driver. If consumer prices for essential goods and services—such as food, housing, energy, and healthcare—continue to rise, then a higher COLA becomes more likely. Economic growth, supply chain dynamics, and global events can all play a role in influencing these price trends. For instance, disruptions in global supply chains can drive up the cost of goods, which then reflects in the CPI-W.

Economic Indicators Influencing COLA

A range of economic indicators are closely watched to predict COLA. These aren’t just abstract numbers; they represent real-world conditions that affect everyone’s wallet. Monitoring these can give you a better sense of where the COLA might land.

- Consumer Price Index (CPI-W): The most direct influence, tracking prices of a basket of goods and services.

- Energy Prices: Fluctuations in oil and gas prices directly impact transportation and manufacturing costs, which filter down to consumers.

- Food Costs: Changes in agricultural output, transportation, and demand significantly affect grocery bills.

- Housing Market Trends: Rent and homeownership costs are major components of household budgets and thus the CPI-W.

The 3.5% projection suggests that economists anticipate these factors will continue to exert upward pressure on prices. While a higher COLA is generally welcomed by beneficiaries, it also underscores the reality of ongoing inflation. This means that while your benefits may increase, the cost of living is also expected to be higher, making careful financial management even more important. It’s a delicate balance where the adjustment aims to keep your purchasing power relatively stable, rather than significantly increasing it in real terms.

Direct Impact on Your Monthly Social Security Benefits

A 3.5% COLA directly translates into an increase in your monthly Social Security benefit payment. For many beneficiaries, this adjustment is a critical component of their financial stability, helping them manage rising living costs. To illustrate, if your current monthly benefit is $1,500, a 3.5% COLA would add $52.50 to your payment, bringing it to $1,552.50. While this might seem like a modest increase individually, collectively across millions of beneficiaries, it represents a substantial injection of funds into the economy.

It’s important to remember that the COLA applies to your primary insurance amount (PIA), which is the benefit you would receive at your full retirement age. Those who claim benefits earlier or later will see their COLA applied to their adjusted benefit amount. The increase is typically reflected in payments starting in January of the adjusted year. This means that if the 3.5% COLA is confirmed for 2026, beneficiaries would see the adjusted amount in their checks or direct deposits beginning that January.

Understanding Your New Benefit Amount

Calculating your new benefit amount is straightforward once the COLA is announced. However, it’s also important to consider other factors that might affect your net payment.

- Multiply Your Current Benefit: Take your current monthly benefit and multiply it by 1.035 (for a 3.5% increase).

- Medicare Part B Premiums: Historically, Medicare Benefits Part B premiums are deducted directly from Social Security benefits. These premiums also tend to increase annually, which can offset some of the COLA increase.

- Income Taxes: Depending on your total income, a portion of your Social Security benefits may be subject to federal income tax. An increase in benefits could potentially push you into a higher tax bracket or make more of your benefits taxable.

While the 3.5% COLA is designed to be a positive adjustment, its real-world impact can be nuanced. Beneficiaries should review their overall financial situation, including other sources of income and expenses, to fully understand how the adjustment will affect their disposable income. The goal is to ensure that the increased benefits genuinely contribute to maintaining or improving your standard of living, rather than simply being absorbed by other rising costs or deductions.

Long-Term Financial Planning with COLA in Mind

Incorporating the projected 3.5% COLA into your long-term financial planning is a prudent step for current and future Social Security beneficiaries. While a COLA provides an annual boost, it’s crucial to view it within the broader context of your overall retirement strategy. Relying solely on COLA increases to cover all future expenses might not be sufficient, given that inflation can sometimes outpace these adjustments, especially for specific categories of goods and services like healthcare.

Financial advisors often recommend a diversified approach to retirement income, combining Social Security with personal savings, investments, and potentially part-time work. The COLA helps maintain the baseline value of your Social Security benefits, but robust financial planning involves anticipating other expenses that may grow at different rates. For instance, healthcare costs, which are a major concern for many retirees, often inflate at a higher rate than the general CPI-W.

Considering the 3.5% COLA for 2026, it’s an opportune moment to re-evaluate your budget and projections. This includes assessing how much of your total income will come from Social Security versus other sources, and how future COLAs might impact that balance. It’s also a good time to review your investment portfolio to ensure it aligns with your long-term goals and risk tolerance, providing complementary growth to your fixed income.

Strategies for Maximizing Your Benefits

Beyond simply receiving the COLA, there are strategies you can employ to make the most of your Social Security benefits and overall retirement finances.

- Delaying Benefits: For every year you delay claiming Social Security past your full retirement age, up to age 70, your benefits increase. These higher initial benefits will then be subject to future COLAs, leading to larger absolute increases.

- Working in Retirement: Continuing to work, even part-time, can not only supplement your income but also potentially increase your future Social Security benefits if your earnings are higher than those in previous years.

- Budgeting and Expense Management: A clear understanding of your monthly expenses allows you to better allocate your increased COLA funds. Prioritizing essential costs and finding ways to reduce discretionary spending can extend the reach of your benefits.

Ultimately, the 3.5% COLA for 2026 serves as a reminder that Social Security is a dynamic system. Proactive financial planning, which factors in these annual adjustments alongside personal savings and investment strategies, is paramount to securing a comfortable and stable retirement. It’s about building a resilient financial framework that can adapt to economic changes and ensure your benefits continue to support your lifestyle.

The Broader Economic Landscape and COLA

The projected 3.5% COLA for 2026 doesn’t exist in a vacuum; it’s a reflection of and a response to the broader economic landscape. Understanding this context helps beneficiaries and policymakers alike appreciate the significance of these adjustments. Factors such as global economic trends, national fiscal policies, and the labor market all play a crucial role in shaping the inflationary environment that dictates COLA rates.

For instance, strong economic growth can sometimes lead to increased consumer demand and higher prices, which would naturally result in a higher COLA. Conversely, an economic downturn might see lower inflation and thus a smaller COLA. Government spending, interest rates set by the Federal Reserve, and even international trade agreements can subtly influence the cost of living for American consumers. These interconnected elements create a complex web that the COLA mechanism attempts to navigate, ensuring benefits retain their value.

Potential Economic Shifts and Their COLA Implications

As we look towards 2026, several potential economic shifts could either reinforce or alter the 3.5% COLA projection. Being aware of these can help you understand the volatility inherent in such forecasts.

- Inflationary Pressures: Persistent supply chain issues, geopolitical events, or strong wage growth could sustain or even increase inflation, potentially leading to a higher COLA.

- Monetary Policy: The Federal Reserve’s decisions on interest rates can influence borrowing costs and consumer spending, impacting inflation. Tighter monetary policy tends to cool inflation.

- Energy Market Volatility: Global oil prices are notoriously volatile. Significant spikes could quickly drive up inflation, while sustained drops could have the opposite effect.

- Labor Market Strength: A robust job market with rising wages can contribute to higher consumer spending and demand, feeding into inflationary cycles.

The 3.5% COLA signals that economists anticipate a continuation of certain inflationary trends. However, the exact figure will only be confirmed after the third-quarter CPI-W data is available. This constant interplay between economic forces means that while projections provide a useful guide, flexibility in financial planning remains essential. The COLA is a testament to the system’s commitment to adapting to economic realities, aiming to provide a stable foundation for beneficiaries amid continuous change.

Navigating Changes: Preparing for 2026 and Beyond

Preparing for the 2026 Social Security adjustments and subsequent years involves a proactive approach to your personal finances. While the 3.5% COLA is a positive step, it’s just one piece of the puzzle. Effective preparation means looking beyond the immediate increase and considering how these changes integrate into your broader financial health. This includes reviewing not only your income but also your expenditure patterns, potential tax implications, and any other benefits you might receive.

One key aspect of preparation is to stay informed. The Social Security Administration provides updates and resources that can help you understand your benefits better. Additionally, consulting with a financial advisor can offer personalized insights into how the COLA and other economic factors might affect your unique situation. They can help you craft a budget, optimize your savings, and make investment decisions that align with your long-term goals, ensuring you’re well-positioned for financial stability.

Key Steps for Beneficiaries

To effectively navigate these changes, beneficiaries can take several concrete steps to ensure they are well-prepared for 2026 and the years that follow.

- Review Your Budget: Reassess your monthly income and expenses to understand how the COLA increase will impact your disposable income. Identify areas where you can save or reallocate funds.

- Check Medicare Premiums: Be aware that Medicare Part B premiums typically increase annually and are often deducted from Social Security benefits, which can offset some of your COLA increase.

- Understand Tax Implications: Consult a tax professional to determine if the increased benefits, combined with other income, could lead to a higher portion of your Social Security being taxable.

- Explore Additional Income Streams: Consider if part-time work, investments, or other savings can supplement your Social Security benefits to better meet your financial needs.

Ultimately, the projected 3.5% COLA for 2026 is an essential adjustment designed to help beneficiaries maintain their purchasing power. However, relying solely on this adjustment without comprehensive financial planning can leave individuals vulnerable to other economic pressures. By taking a proactive and informed approach, you can ensure that the Social Security adjustments work effectively within your overall financial strategy, providing greater peace of mind and security for your future.

| Key Aspect | Brief Description |

|---|---|

| 3.5% COLA Projection | Anticipated Cost-of-Living Adjustment for Social Security benefits in 2026. |

| Inflation Offset | COLA aims to protect beneficiaries’ purchasing power against rising living costs. |

| Benefit Increase | Directly adds to monthly Social Security payments starting January 2026. |

| Financial Planning | Crucial to integrate COLA into overall retirement budget, considering taxes and Medicare. |

Frequently Asked Questions About 2026 Social Security Adjustments

The primary purpose of the Social Security Cost-of-Living Adjustment (COLA) is to counteract the effects of inflation. It ensures that the purchasing power of Social Security benefits remains stable over time, allowing beneficiaries to maintain their standard of living despite rising costs for goods and services.

The 2026 COLA will be calculated by comparing the average Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from July, August, and September of 2025 to the average CPI-W from the same months of 2024. The percentage increase determines the COLA.

A 3.5% COLA will increase your gross Social Security benefit. However, the net increase might be partially offset by other factors like rising Medicare Part B premiums, which are often deducted directly from benefits, and potential increases in income tax liability depending on your total income.

The official announcement for the 2026 Social Security COLA typically occurs in mid-October of 2025. This timing allows the Social Security Administration to gather and process the necessary third-quarter CPI-W data to finalize the adjustment percentage.

To prepare, review your current budget, assess how the COLA might affect your overall income, and consider potential impacts from Medicare premium increases or tax changes. Consulting a financial advisor can provide tailored strategies for your specific financial situation.

Conclusion

The anticipated 3.5% Cost-of-Living Adjustment for 2026 signifies a crucial development for millions of Social Security beneficiaries. This adjustment, driven by inflationary trends, is designed to help maintain the purchasing power of benefits, offering a necessary financial boost. While the increase is a positive step, it underscores the importance of comprehensive financial planning that extends beyond just the COLA. By understanding the mechanisms behind these adjustments, actively managing personal finances, and staying informed about broader economic factors, beneficiaries can strategically position themselves to navigate the evolving financial landscape, ensuring greater security and stability in their retirement years and beyond.

formulas raises questions")