Fed’s 2026 Outlook: 50 BPS Hike & National Borrowing Impact

Anúncios

A potential 50 basis point Federal Reserve rate hike in 2026 could significantly alter national borrowing costs, impacting government debt, corporate financing, and consumer loans, with ripple effects across the U.S. economy.

The financial landscape of the United States is constantly evolving, influenced heavily by the actions of the Federal Reserve. As we look towards 2026, discussions around a potential Federal Reserve’s 2026 Outlook: What a Potential 50 Basis Point Rate Hike Means for National Borrowing (FINANCIAL IMPACT) are gaining traction. Understanding the implications of such a move is crucial for policymakers, businesses, and individual citizens alike, as it directly affects the cost of money and, consequently, the nation’s ability to borrow and grow.

Anúncios

Understanding Federal Reserve Rate Hikes

The Federal Reserve, often referred to as the Fed, serves as the central banking system of the United States. Its primary mandate includes maintaining maximum employment, stable prices, and moderate long-term interest rates. To achieve these goals, the Fed utilizes various monetary policy tools, with adjusting the federal funds rate being one of the most powerful and closely watched.

Anúncios

A rate hike, specifically a 50 basis point (0.50%) increase, signals the Fed’s response to economic conditions, typically to curb inflation or cool down an overheating economy. When the Fed raises this benchmark rate, it influences a cascade of other interest rates throughout the economy, from prime lending rates to mortgage rates and the yield on government bonds. This ripple effect makes borrowing more expensive for everyone, from the federal government to individual consumers.

The Mechanism of a Rate Hike

When the Federal Open Market Committee (FOMC) decides to raise the federal funds rate, it essentially increases the cost for banks to borrow money from each other overnight. This increased cost is then passed on to consumers and businesses in various forms.

- Increased Lending Costs: Banks face higher borrowing costs, leading them to raise their own lending rates for mortgages, auto loans, and credit cards.

- Impact on Government Debt: The Treasury must offer higher yields on new debt issuances to attract investors, increasing the cost of financing the national debt.

- Investor Behavior Shift: Higher rates can make fixed-income investments more attractive, potentially drawing capital away from riskier assets like stocks.

The decision to implement a 50 basis point hike is not taken lightly and typically reflects a significant concern about inflationary pressures or a robust economy that can withstand higher borrowing costs without stifling growth. Such a move indicates a determined effort by the Fed to steer the economy towards its long-term objectives, often with a focus on price stability.

Direct Impact on Government Borrowing

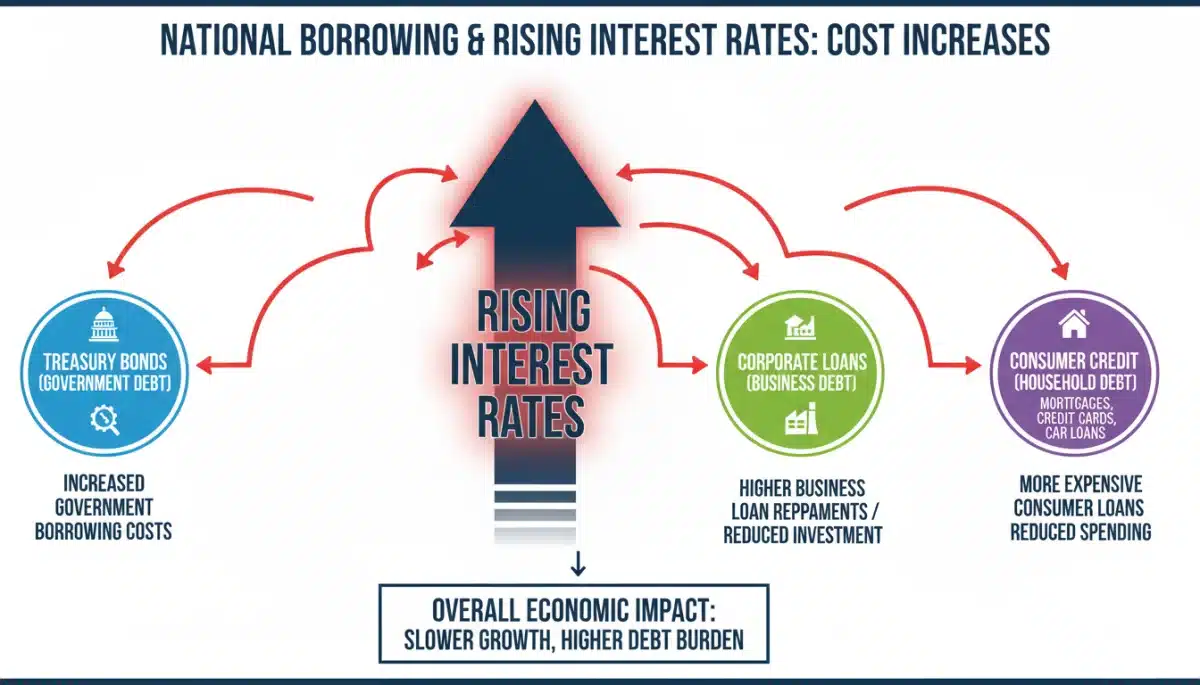

The federal government is the largest borrower in the United States, constantly issuing new debt to finance its operations, programs, and existing obligations. A 50 basis point rate hike by the Federal Reserve carries substantial implications for the cost of this national borrowing, potentially adding billions to the annual interest payments on the national debt.

When interest rates rise, the Treasury Department must offer higher yields on newly issued government bonds, notes, and bills to remain competitive and attract investors. This directly translates into increased interest expenses for the government. With a national debt already in the tens of trillions, even a seemingly small increase in interest rates can have a magnified effect on the federal budget, diverting funds that could otherwise be used for public services or investments.

Increased Cost of Servicing the National Debt

The sheer scale of the national debt means that a 0.50% increase in borrowing costs can equate to tens of billions of dollars in additional annual interest payments. This burden can constrain fiscal policy, limiting the government’s flexibility in responding to economic downturns or funding new initiatives.

- Budgetary Constraints: Higher interest payments consume a larger portion of the federal budget, potentially leading to cuts in other areas or increased taxes.

- Investor Demand: While higher yields attract investors, persistent increases could signal underlying economic instability, affecting long-term demand for U.S. debt.

- Refinancing Challenges: As existing debt matures, it must be refinanced at the new, higher rates, compounding the interest burden over time.

Moreover, the perception of the U.S. government’s ability to manage its debt can influence international confidence. While the U.S. dollar remains a global reserve currency, sustained increases in debt servicing costs could, in extreme scenarios, raise questions about fiscal sustainability, though this is a long-term risk rather than an immediate one. The direct consequence is a tighter federal budget and less room for maneuver.

Effects on Corporate and Business Borrowing

Businesses, from small startups to multinational corporations, rely heavily on borrowing to fund their operations, expansion plans, and capital investments. A 50 basis point rate hike by the Federal Reserve would significantly increase the cost of corporate borrowing, influencing investment decisions, profitability, and overall economic growth.

When the federal funds rate rises, commercial banks typically adjust their prime lending rates upwards, which directly impacts the interest rates on corporate loans, lines of credit, and bond issuances. This means companies will face higher expenses when taking out new loans or refinancing existing debt. For businesses operating on thin margins, these increased costs can be a critical factor in their ability to invest, hire, and innovate.

Challenges for Business Expansion and Investment

Higher borrowing costs can deter companies from embarking on new projects or expanding their operations. This can lead to a slowdown in capital expenditure and job creation, potentially dampening economic dynamism. Businesses might prioritize debt reduction over growth, affecting overall market sentiment.

- Reduced Investment: Fewer new projects and expansions due to higher financing costs.

- Lower Profit Margins: Increased interest expenses can erode profitability, especially for highly leveraged companies.

- Credit Crunch Risk: Banks might become more cautious in lending, tightening credit availability for some businesses.

Furthermore, smaller businesses and startups, which often have less access to diverse funding sources and are more reliant on traditional bank loans, may feel the pinch more acutely. Their ability to secure affordable financing is crucial for their survival and growth, and a significant rate hike could pose considerable challenges. Large corporations, while potentially having more options, will also see their financing costs rise, affecting their balance sheets and shareholder returns.

Consumer Borrowing: Mortgages, Loans, and Credit

The average American consumer is acutely sensitive to changes in interest rates, as these directly affect the cost of their mortgages, auto loans, credit card debt, and personal loans. A 50 basis point Federal Reserve rate hike would translate into higher monthly payments and greater financial burdens for many households, influencing spending habits and overall economic activity.

Mortgage rates, which are often tied to the yield on long-term Treasury bonds, would likely see an upward adjustment. For prospective homebuyers, this means higher monthly mortgage payments, potentially reducing affordability and cooling down the housing market. Existing homeowners with adjustable-rate mortgages (ARMs) would also experience an increase in their payments, placing additional strain on their budgets.

Impact on Household Budgets and Spending

Beyond mortgages, other forms of consumer credit would also become more expensive. Auto loan rates would rise, making new car purchases pricier. Credit card interest rates, which are frequently variable, would also increase, adding to the burden of revolving debt. Personal loans, often used for consolidating debt or unexpected expenses, would also carry higher costs.

- Higher Mortgage Payments: Increased costs for new home buyers and those with adjustable-rate mortgages.

- Increased Auto Loan Expenses: New vehicle purchases become more expensive, potentially impacting demand.

- Credit Card Debt Burden: Higher interest rates on revolving credit can make it harder for consumers to pay down debt.

The collective effect of these increased borrowing costs could lead to a reduction in discretionary spending, as households allocate a larger portion of their income to debt servicing. This contraction in consumer spending, which is a major driver of the U.S. economy, could slow down economic growth. Consumers may become more cautious, delaying large purchases and focusing on savings, further impacting various sectors of the economy.

Economic Implications and Market Reactions

A 50 basis point rate hike by the Federal Reserve in 2026 is not an isolated event; it sends powerful signals through the financial markets and has broad economic implications. The move would likely be interpreted as a strong commitment by the Fed to combat inflation, even if it means slowing down economic growth to some extent. Market reactions would be swift, impacting everything from stock valuations to currency exchange rates.

Equity markets typically react negatively to higher interest rates, as increased borrowing costs can reduce corporate profits and make fixed-income investments more attractive by comparison. This could lead to a sell-off in stocks, particularly in growth sectors that rely heavily on future earnings potential. Conversely, the U.S. dollar might strengthen as higher interest rates make dollar-denominated assets more appealing to international investors, potentially impacting trade balances.

Market Volatility and Investor Sentiment

The announcement of such a significant rate hike could introduce volatility into the markets as investors adjust their portfolios to the new economic reality. Sectors that are highly sensitive to interest rates, such as real estate and utilities, might experience more pronounced impacts. Investor sentiment would likely shift towards a more conservative stance, prioritizing stability over aggressive growth.

- Stock Market Correction: Potential for equities to decline as higher rates impact corporate earnings and valuation multiples.

- Stronger Dollar: Increased demand for dollar-denominated assets could lead to currency appreciation, affecting exports.

- Bond Market Adjustment: Yields on existing bonds would adjust to reflect the new interest rate environment, potentially leading to capital losses for some bondholders.

Furthermore, the hike could influence global capital flows, as investors seek higher returns in the U.S. market, potentially impacting emerging economies. The Fed’s actions are closely watched by central banks worldwide, and a significant rate hike could prompt similar adjustments in other countries, creating a synchronized global tightening of monetary policy. This intertwining of economic policies underscores the far-reaching influence of the Federal Reserve.

Navigating the Future: Strategies for Adaptation

In anticipation of a potential 50 basis point rate hike in 2026, various stakeholders—from the federal government and corporations to individual consumers—will need to adapt their financial strategies. Proactive planning can mitigate the adverse effects of higher borrowing costs and potentially even uncover new opportunities in a changing economic landscape.

For the federal government, this means a renewed focus on fiscal responsibility and debt management. Exploring strategies to reduce reliance on short-term borrowing and extending the maturity of outstanding debt could help buffer the impact of rising interest rates. Policymakers might also need to prioritize spending and revenue generation to maintain fiscal stability in the face of increased interest expenses.

Recommendations for Businesses and Consumers

Businesses should review their debt structures, considering refinancing options before rates climb further and focusing on improving operational efficiency to absorb higher financing costs. Consumers, on the other hand, should prioritize paying down high-interest debt, such as credit card balances, and carefully evaluate the affordability of new loans.

- Government: Focus on fiscal discipline, debt maturity management, and revenue optimization.

- Corporations: Evaluate debt portfolios, consider refinancing, and enhance operational efficiency.

- Consumers: Prioritize high-interest debt repayment, build emergency savings, and reassess borrowing needs.

Moreover, individuals might consider locking in fixed-rate loans for major purchases, like mortgages, if they anticipate further rate increases. Investing in financial education and seeking professional advice can also empower individuals and businesses to make informed decisions. The ability to adapt and innovate in response to evolving monetary policy will be key to navigating the financial challenges and opportunities that a rate hike might present.

The Broader Economic Landscape in 2026

The Federal Reserve’s potential 50 basis point rate hike in 2026 must be viewed within the broader economic landscape, which will be shaped by numerous factors beyond monetary policy. Geopolitical developments, global supply chain dynamics, technological advancements, and domestic policy decisions will all play a significant role in determining the overall health and direction of the U.S. economy.

While a rate hike aims to stabilize prices, its effectiveness will depend on how these other variables interact. For instance, persistent global supply chain disruptions could counteract the Fed’s efforts to control inflation, while strong technological innovation could drive productivity and growth, helping to offset the dampening effects of higher borrowing costs. The labor market, consumer confidence, and business investment trends will also be crucial indicators to watch.

Interconnectedness of Economic Factors

The economy is a complex system, and a rate hike is just one piece of the puzzle. Understanding the interconnectedness of various economic factors will be essential for forecasting the full impact of the Fed’s actions. Policymakers will need to remain agile, adjusting their strategies in response to real-time data and unforeseen events.

- Global Influences: Geopolitical stability, international trade policies, and global economic growth will affect the U.S. economy.

- Technological Progress: Innovations in AI, automation, and green energy could reshape industries and productivity.

- Fiscal Policy: Government spending, taxation, and regulatory changes will complement or contrast monetary policy.

Ultimately, the Federal Reserve’s decision to raise rates is a strategic move to guide the economy towards sustainable growth and price stability. However, the path to 2026 will undoubtedly be influenced by a dynamic interplay of domestic and international forces. Adapting to these changes, both at a macroeconomic and microeconomic level, will be paramount for ensuring continued prosperity and financial resilience.

| Key Point | Brief Description |

|---|---|

| Government Borrowing Costs | A 50 BPS hike significantly increases the cost of servicing the national debt, impacting the federal budget. |

| Corporate Loan Expenses | Businesses face higher interest rates on loans, potentially slowing investment and expansion. |

| Consumer Debt Burden | Mortgages, auto loans, and credit card interest rates rise, impacting household budgets and spending. |

| Market Reactions | Equity markets may decline, while the U.S. dollar could strengthen, influencing global capital flows. |

Frequently Asked Questions About Fed Rate Hikes

A basis point (BPS) is a common unit of measure for interest rates and other financial percentages. One basis point is equal to one-hundredth of a percentage point (0.01%). Therefore, a 50 basis point rate hike means an increase of 0.50% in the federal funds rate.

If you have a fixed-rate mortgage, a rate hike would not immediately affect your payments. However, for those with adjustable-rate mortgages (ARMs), payments could increase relatively quickly, typically after the next scheduled adjustment period, reflecting the new market rates.

Yes, typically. Higher interest rates can make borrowing more expensive for companies, potentially reducing their profits and making fixed-income investments more attractive. This often leads to a short-term negative reaction in the stock market, though long-term impacts vary.

The Federal Reserve primarily raises interest rates to combat inflation and ensure price stability. By making borrowing more expensive, the Fed aims to cool down an overheating economy, reduce demand, and bring inflation back to its target long-term rate, typically around 2%.

A rate hike increases the cost for the U.S. Treasury to issue new debt and refinance existing debt. This means the government will have higher interest payments on its national debt, potentially impacting the federal budget and limiting fiscal flexibility for other spending initiatives.

Conclusion

The prospect of a 50 basis point Federal Reserve rate hike in 2026 underscores the dynamic nature of the U.S. economy and the critical role of monetary policy in shaping its trajectory. Such a move, while aimed at fostering long-term price stability, would undoubtedly introduce significant shifts in national borrowing costs, impacting everything from the federal budget to corporate investment and individual household finances. Navigating this evolving landscape will require foresight, strategic adaptation, and a keen understanding of the interconnected economic forces at play. As we move closer to 2026, staying informed about these potential changes will be paramount for all stakeholders.